Regulation is a Key Driver of the Clean Shipping Transition

By: Nicole Gotthardt & Berta Lascuevas Laguna

The background image at the top of this article belongs to Everllence.

What current maritime decarbonization standards drive market change in the sector, and how do they work? As international supply chains come under increasing pressure to decarbonize, attention is shifting from whether the sector must change to how fast and by what means the transition will occur. At the Carbon Containment Lab, we focus on directing this urgency towards action by applying scientific, entrepreneurial, and investment expertise to accelerate scalable climate solutions. Through rigorous evaluation of the carbon intensity of emerging fuel pathways, we aim to bridge the gap between regulatory ambition and deployable, real-world decarbonization strategies. In this post, we outline the leading regulations driving shipping decarbonization—including those by the International Maritime Organization (IMO) and the European Union (EU)—and highlight key challenges that must be addressed to translate policy ambition into real-world impact.

See our previous post here for the connection between black carbon emissions and clean marine fuels, and our Methane-to-Methanol project page for more information on our current work.

Maritime is a Hard-to-Abate Sector Under Pressure to Decarbonize

International shipping is a major emitter of global greenhouse gas (GHG) emissions, reaching approximately 1.1 billion tons of carbon dioxide equivalents (CO2e) in 2018, around 2.9% of global emissions.[1] Decarbonization efforts in the marine shipping industry began emerging in the mid-2000s, initially driven by growing demand for lower-carbon options. Increasing attention to climate change mitigation—along with investor pressure and consumer demand—prompted major clients of the shipping sector, including retailers, manufacturers, and commodity traders, to pursue lower-carbon supply chains as part of their corporate sustainability commitments. As awareness of the sector’s emissions footprint grew, regulators followed by introducing policies to guide the transition.

Today, the transition to low-carbon shipping is shaped by a mix of national, regional, and global policies. Several countries, including the United Kingdom, Norway, and Singapore, are advancing this shift through establishing decarbonization regulations, funding innovation in technology development, and creating initiatives like green shipping corridors. While these national efforts are crucial, global and supranational regulatory frameworks—such as those deployed by the IMO and EU—are the primary global regulatory drivers of maritime decarbonization. Both the IMO and EU have committed to achieving net-zero emissions from shipping by 2050 and have implemented mechanisms that penalize high emitters while rewarding early adopters of cleaner fuels.

The Regulations Steering Decarbonization

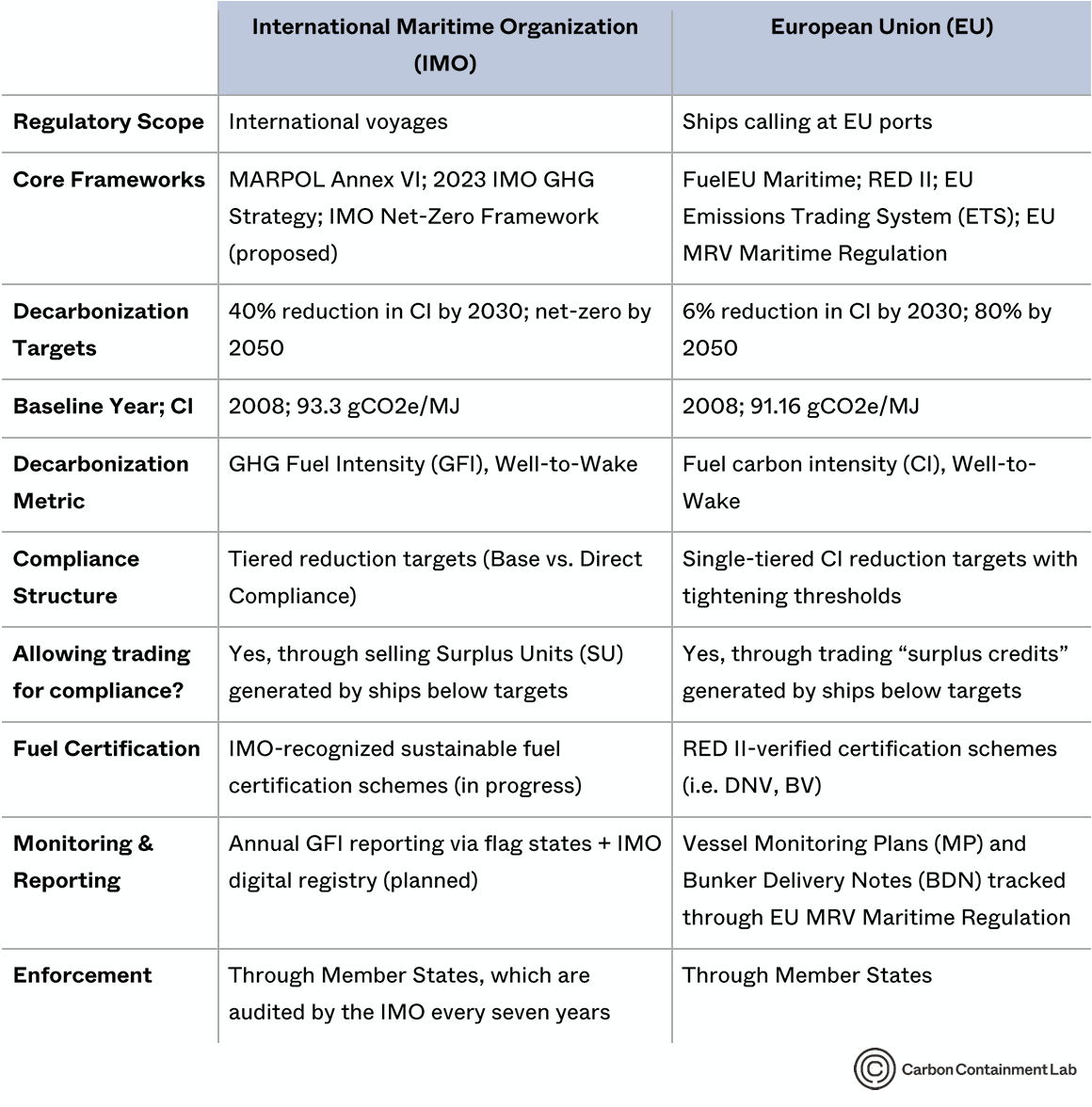

Although the IMO and EU regulate shipping through different jurisdictions and regulatory mechanisms, their frameworks share a common architecture: they set life cycle-based emissions reduction targets for marine fuels, require monitoring and reporting, and impose financial incentives and penalties to drive compliance. Table 1 compares these frameworks, highlighting where the two approaches align and where key differences in scope, timelines, and enforcement emerge.

The IMO Framework: Global Standards for Shipping

The IMO regulates pollution and GHG emissions from international shipping through three main regulatory frameworks: i) the International Convention for the Prevention of Pollution from Ships (MARPOL), ii) the 2023 IMO GHG Strategy, and iii) the IMO Net Zero Framework.

MARPOL is the cornerstone of global shipping environmental regulation. Adopted under the IMO, MARPOL is an international treaty that has been ratified by a majority of the world’s maritime nations. By joining the treaty, countries agree to implement and enforce its rules on their ships, giving the IMO legal force across international shipping.

One of the treaty’s key components, Annex VI, regulates air pollution (including GHGs) from ships. It sets limits on sulfur oxide (SOx) and nitrogen oxide (NOx) emissions; bans the use of ozone-depleting substances; and designates stricter standards for SOx, NOx, and particulate matter (PM) in certain geographic zones, called Emission Control Areas (ECAs).[2] Annex VI also establishes mandatory technical and operational efficiency measures aimed at reducing GHG emissions from ships. All of the IMO’s climate regulations are incorporated into this Annex as formal amendments, making them legally binding.

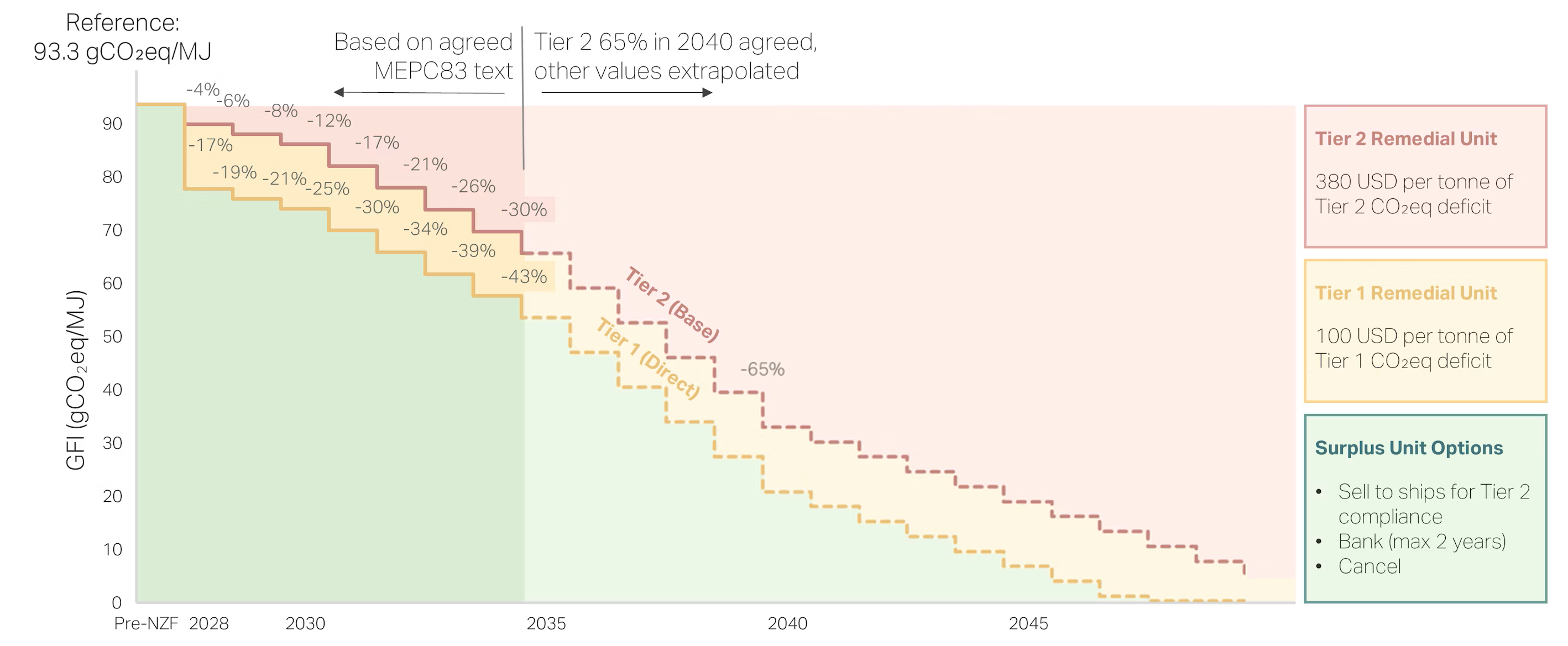

The 2023 IMO GHG Strategy sets the future vision for international shipping through policies designed to accelerate the shift to cleaner fuels and more efficient vessels. The strategy establishes four core ambitions: i) reaching net-zero Well-to-Wake (WtW)—accounting for emissions across the full fuel life cycle, from production to onboard use—shipping by 2050; ii) improving vessel energy efficiency to reduce individual ship carbon intensity (CI); iii) reducing the GHG fuel intensity (GFI) of international shipping; and iv) accelerating the uptake of zero- or near-zero emission fuels and technologies with a target for at least 5% of shipping energy to stem from these sources by 2030.[3] The 2023 strategy also sets a separate carbon intensity target, requiring a 40% reduction by 2030 compared to a 2008 baseline of 93.3 grams of CO2-equivalent per megajoule (gCO2e/MJ).

While the 2023 IMO GHG strategy sets the decarbonization targets, the IMO Net-Zero Framework (NZF) is the proposed regulatory framework designed to achieve them. If adopted, the NZF will require large ocean-going ships (>5,000 gross tonnage (GT)) participating in international voyages to reduce their GFI annually.[4] To accomplish this, the NZF establishes an incentive framework, where over-emitting ships must pay to balance their deficit emissions, and those using clean fuels are eligible for financial rewards.

Ships will be required to reduce their GFI annually at a predefined percentage (see Figure 1).[5] The GFI represents the weighted average emission intensity of the energy consumed over a year on a WtW basis, and covers carbon dioxide (CO2), methane (CH4), and NOx. The GFI is calculated through the methods defined in the IMO 2024 LCA Guidelines.[6] GFI reduction targets steadily decline from the IMO 2008 baseline, and are structured in two levels: a “Base Target” (Tier 2) and a “Direct Compliance Target” (Tier 1) (see Figure 1). The IMO has established GFI reduction targets for both levels for the period 2028 to 2035, and a 2040 Base Target of 65% reduction from the baseline (represented by the orange [base] and green [compliance] lines in Figure 2). The remaining targets will be defined by 2032.

Large ships are currently required to monitor and report fuel consumption, distance travelled, and hours spent in motion through the IMO Data Collection System (DCS).[7] If the NZF is adopted, these vessels would also be required to report auxiliary emissions and GFI, submitting data to their flag state annually. Fuel emissions and sustainability claims would be independently verified through a Sustainable Fuel Certification Scheme recognized by the IMO’s Marine Environment Protection Committee (MEPC). These verified schemes will be named in the upcoming IMO negotiations, which take place in April and October every year. A new digital IMO GFI Registry will be established to track the compliance status of individual vessels, recording surplus units (SU) banked and remedial units (RU) acquired, GFI calculations, and transfer and cancellation records. Member States are responsible for the enforcement of IMO regulations and are audited approximately every seven years to ensure compliance.

Figure 1: IMO Net-Zero Framework's Two-Tiered GFI Reduction Pathways

The EU Framework: A Supranational Regulatory Framework

The EU regulates ships that travel to or from ports within the EU and in European waters through four primary regulations: i) FuelEU Maritime, ii) Renewable Energy Directive (RED) II; iii) EU Monitoring, Reporting, and Verification (MRV) Maritime Regulation, and iv) the EU Emissions Trading Scheme (ETS).

FuelEU Maritime is the EU’s primary regulation for limiting the GHG intensity of energy used in vessels calling at European ports, regardless of their flag.[8] Ships above 5,000 gross tonnage are required to decrease the GHG intensities of the fuel and energy used over time, cutting the CI by 2% by 2025, 6% by 2030, and 80% by 2050, compared to a 2008 baseline of 91.16 gCO2e/MJ (represented by the blue line in Figure 2).[9] Reduction targets cover CO2, CH4, and N2O over the full life cycle of fuels used onboard, on a WtW basis. The restrictions apply to all energy used during voyages within the EU and in port, and up to 50% of the energy used on trips entering, leaving, or involving an outermost region of the EU. To prevent air pollution in ports, FuelEU also sets obligations for container ships and passenger ships to use on-shore power supply (OPS) or alternative zero-emission technologies from January 1st, 2030, in heavily-trafficked ports (>100 annual container ship calls, covered under article 9 of the Alternative Fuels Infrastructure Regulation).

FuelEU Maritime provides default emission factors for marine fuels, but relies on the fuel certification framework outlined in the RED II. RED II is a standard that defines sustainability and fuel criteria for low-carbon fuels, establishing acceptable low-carbon fuel pathways and life-cycle emission calculations on a WtW basis.[10] Article 29 of RED II establishes a life cycle methodology for calculating the CI of marine fuels, assigning emissions values to each feedstock and production pathway using either default values or verified measured data.

Fuels must be verified through recognized sustainability schemes—such as the International Sustainability and Carbon Certification (ISCC) or the Roundtable on Sustainable Biomaterials (RSB)—to qualify under RED II. To use certified GHG values, sustainable fuels must meet minimum savings compared to the baseline: 50–60% for non-food and feed crop biofuels and 70% for all other fuels.

Beginning January 1st, 2025, individual ships report compliance through the EU MRV Maritime Regulation, which establishes reporting structures that include vessel monitoring plans (MP) authorized by National Accreditation Bodies (NABs) of EU Member States, such as DNV (Det Norske Veritas) or Bureau Veritas (BV).[11] By April 20th of each year, companies must submit verified emissions reports to the Commissions and States and keep a document of compliance.

Alongside requiring a reduction in the CI of marine fuels, the EU also implements a carbon penalty through its Emissions Trading Scheme (ETS).[12] The EU ETS is a cap-and-trade carbon market that covers CO2, CH4, and N2O emissions from all large ships (>5,000 gross tonnage) entering EU ports, regardless of their flag. The ETS covers 50% of emissions starting or ending outside the EU and 100% of emissions that occur between two EU ports. Vessels must purchase and surrender EU allowances for their direct GHG emissions on voyages for each ton of reported CO2e. Under the ETS phase-in, ships must surrender allowances for 40% of emissions reported in 2024 in 2025, 70% of emissions reported in 2025 in 2026, and 100% of emissions from 2027 onwards.

-1777573236.png)

Inside the Incentive Frameworks

Both the IMO and EU have a cost of non-compliance in their maritime frameworks. Ships that fail to meet GHG-intensity targets face penalties associated with their excess emissions. Under the IMO NZF, vessels that do not meet their targets are in compliance deficit and must purchase Remedial Units (RUs), which are priced at two levels depending on the amount of CO2e deficit. Ships that exceed the less stringent Base Target face a penalty of $380 per ton of CO2e deficit, while vessels emitting above the more ambitious Direct Compliance Target but below the Base Target face a lower penalty of $100 per ton of CO2e (see Figure 1).[13] FuelEU Maritime penalizes vessels that exceed their allowed emissions intensity at a fixed rate of €2,400 per ton of very-low-sulfur-oil (VLSFO) equivalent excess fuel.[14]

Importantly, both frameworks allow for the trading of compliance credits. Ship owners with the financial and technical capacity to transition to low-carbon fuels can generate surplus credits and sell them to operators for whom retrofits or fuel-switching remain cost-prohibitive. In the IMO NZF, ships that emit below their targets generate Surplus Units (SUs). These credits can be transferred to vessels with a Base Target compliance deficit, banked for up to two future reporting periods, or voluntarily cancelled and sold into the Voluntary Carbon Market. For FuelEU Maritime, ships that exceed their annual GHG intensity reduction target similarly generate surplus credits, which can be banked for future compliance periods, traded between ships and companies via pooling agreement, or borrowed from the next reporting period in certain circumstances.[15]

Barriers to Policy Implementation

The delay of IMO NZF has substantially slowed progress and certainty of maritime decarbonization efforts. In October 2025, member states of the Marine Environmental Protection Committee (MEPC) voted to adjourn the adoption of the NZF for one year. Disagreements on unresolved technical and structural issues—including incomplete life cycle assessment guidelines, uncertainty around the governance and operation of the Net-Zero Fund, and limited availability of low-carbon fuels—were amplified by geopolitical tensions and led to the delay. If adopted at the next MEPC meeting, the earliest the NZF can enter into force is March 2028. While the formal adoption was delayed, working groups continue advancing the framework by establishing criteria for fuel certification schemes and strengthening LCA methodologies.

It is unclear whether the NZF will garner enough support for adoption in the next few years. Uncertainty in the adoption timeline, or adoption in general, has introduced substantial unpredictability for shipowners, fuel suppliers, and investors, who rely on a stable market to make future vessel and fuel decisions. Shipping companies order new vessels 3-5 years in advance, and currently do not know what the fuel supply landscape or incentive structures will look like, making their decisions difficult.

If adopted, the IMO NZF would introduce added complexity through jurisdictional overlap with FuelEU Maritime. While the IMO sets global standards for ships operating between countries, FuelEU Maritime applies to vessels calling at EU ports. These frameworks have different decarbonization timelines, emissions metrics, and MRV requirements. Compliance with both would require shipowners to undergo double monitoring and reporting, increasing administrative burden and costs. FuelEU Maritime does include a provision to sunset if an equally stringent international regime is implemented; however, its deep integration within the EU regulatory system makes this unlikely.

Beyond Policy: The Shift to Low-Carbon Fuels

Decarbonization policy plays a critical role in driving the demand for cleaner fuels. By establishing specific emissions-reduction targets, regulators like the IMO and EU create a clear trajectory for how quickly the shipping sector must decarbonize. Targets alone, however, do not transform fuel markets. The shift towards low-carbon fuels occurs due to the penalties attached to non-compliance. When regulations impose a financial cost on the continued use of carbon-intensive fuels, they alter the economics of fuel choice, making it increasingly expensive to rely on fossil fuels and effectively narrowing the price gap between conventional and low-carbon alternatives.

However, this price signal is only effective in a robust and stable policy environment; fragmented regulations, delayed global alignment, and overlapping jurisdictions create uncertainty that slows green investment and complicates decision-making. Ultimately, while policy sets the direction, it is the availability, scalability, and cost of alternative fuels that will determine how—and how fast—shipping can decarbonize. In the next post, we turn to that question directly, unpacking the emerging landscape of alternative marine fuels and what it means for the future of global shipping.