A current snapshot of the voluntary and compliance market cooling-related emissions reduction projects.

Snapshot of Today’s Cooling Carbon Market

Today, carbon markets help finance and accelerate efforts to mitigate cooling super pollutant gases, but their full potential is yet to be realized. This report aims to provide a data-driven overview of the cooling markets, highlighting cooling-specific market trends on methodologies, credit issuances, and credit retirements.

A total of 120,110,411 (~120M) cooling-related carbon credits were issued between 2009 and 2025. This represents some 24% of the total super pollutant carbon credits and 4.7% of all voluntary carbon markets and compliance credits in the same period.

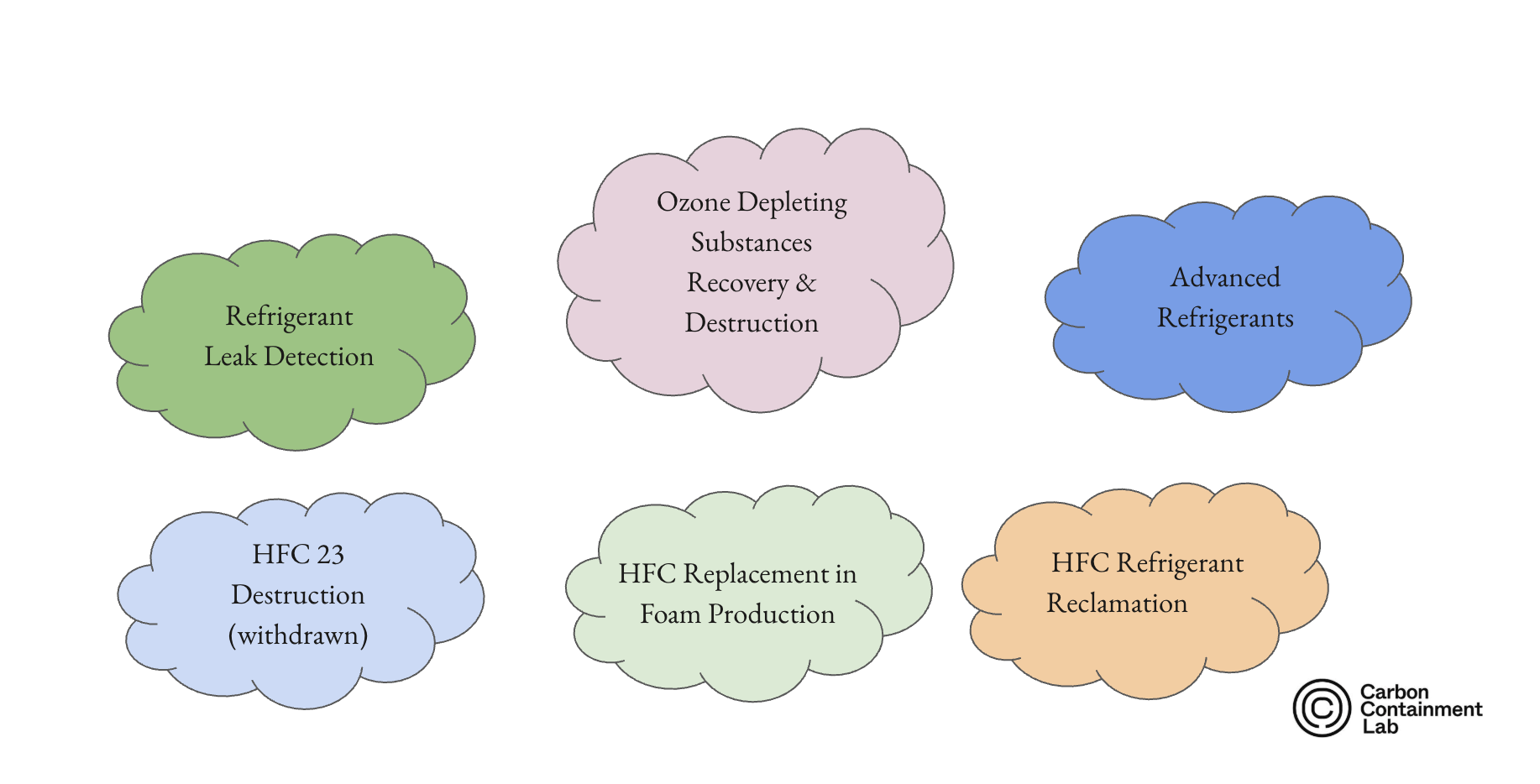

The data covers both global voluntary carbon markets as well as U.S. compliance markets from 2009 to the end of 2025. The data is primarily based on the UC Berkeley Voluntary Registry Offsets Database (v2025-12-year-end), which gathers and organizes data from major registries (ACR, CAR, Gold Standard, and Verra). We supplemented this data with additional data from other registries and sources (i.e., Oneshot.Earth’s Open Carbon Protocol, Isometric, Global Heat Reduction Initiative and The UN Environment Programme’s Article 6 Pipeline). Notably, not all of these methodologies and credits are still active. For example, HFC-23 destruction credits have been withdrawn. We classify these methodologies into six key cooling-related project types, as shown in Figure 1.

Figure 1: Six types of cooling emissions mitigation projects supported by carbon markets

Several limitations should be noted when interpreting the findings of this report. First, the analysis relies exclusively on publicly available registry data and therefore does not capture private offtake agreements or bilateral transactions that may materially affect credit availability and demand dynamics. Second, several registries and methodologies included in the analysis are relatively new and have not yet published comprehensive or consistent historical data, which may lead to an underrepresentation of emerging activity. Pricing data is not included as this is not published in any consistent format and is often undisclosed by parties. This limits our ability to assess price dispersion as well as the relationship between supply growth and demand signals. Finally, there are of course a wide range of cooling-related emission reduction activities not all suited to carbon credit finance. We do not describe these emission reduction and energy saving activities in this report.

Methodologies

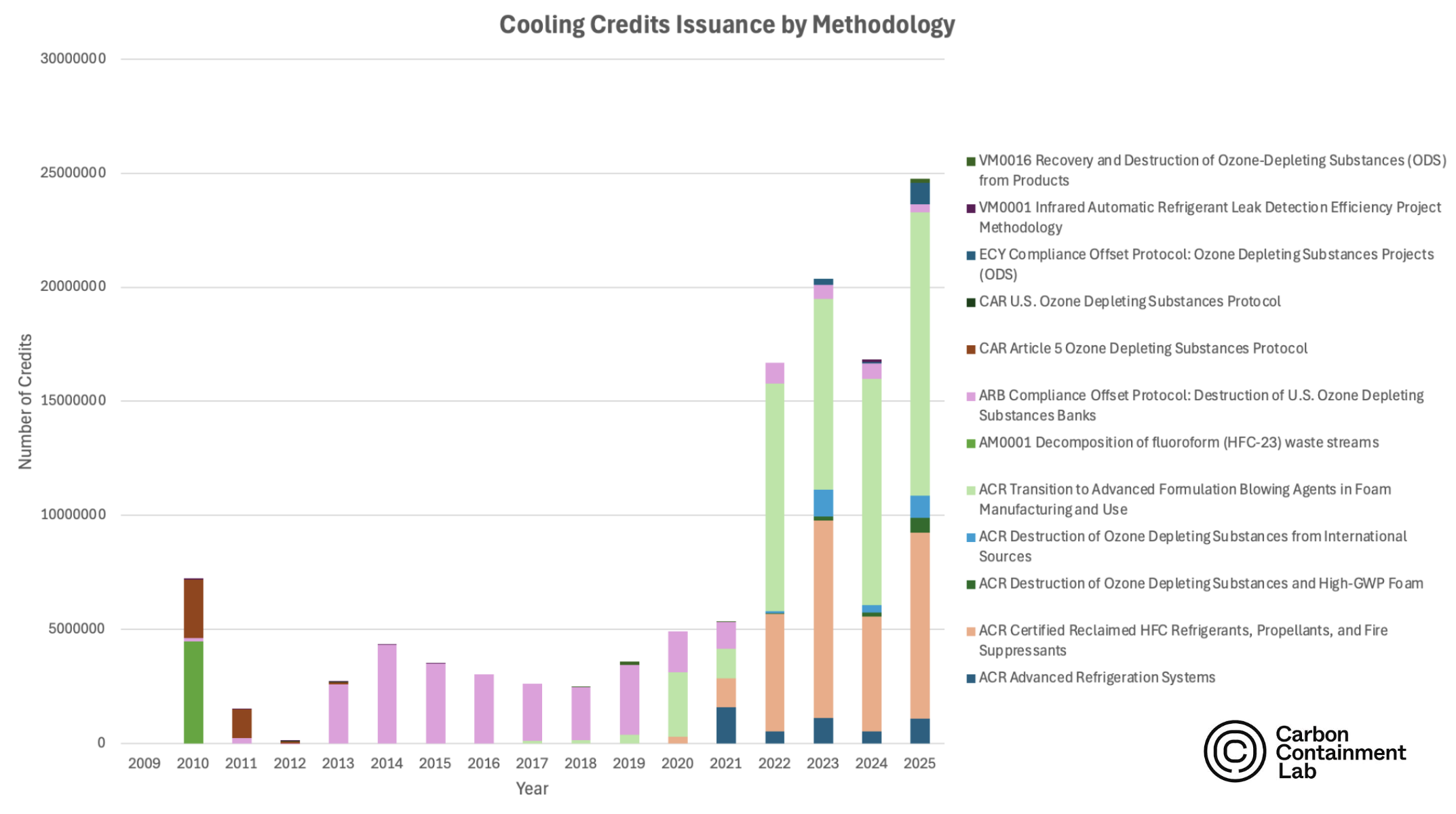

Today, there are 12 published methodologies on three voluntary carbon market registries. There are an additional four methodologies in compliance markets, one in Article 6, one from the Global Heat Reduction Initiative, and one from OneShot.Earth. There are at least two more methodologies currently in draft form that are expected to be released in 2026 (by the Open Carbon Protocol and Isometric). The total number of credits (measured by metric tonnes of CO2 equivalent, or MTCO2e) issued by each of these methodologies by year is shown in Figure 2.

Figure 2. Cooling Credits Issued by Methodology and Year

Total cooling credit issuance is overwhelmingly driven by a narrow subset of methodologies, particularly “ACR Transition to Advanced Formulation Blowing Agents in Foam Manufacturing and Use” and “ACR Certified Reclaimed HFC Refrigerants, Propellants, and Fire Suppressants”. Together, these two methodologies account for over 74 million credits, representing a dominant share of total issuance across all protocols listed.

While legacy compliance frameworks such as “ARB Compliance Offset Protocol: Destruction of U.S. ODS Banks” remain significant (27.2 million credits across 258 projects), several ACR voluntary methodologies now match or exceed compliance protocols in total issued volume with far fewer projects.This indicates a structural transition in the cooling credit market: issuance leadership has shifted away from compliance-anchored ODS bank destruction toward voluntary methodologies that can scale through ongoing industrial, lifecycle refrigerant management processes.

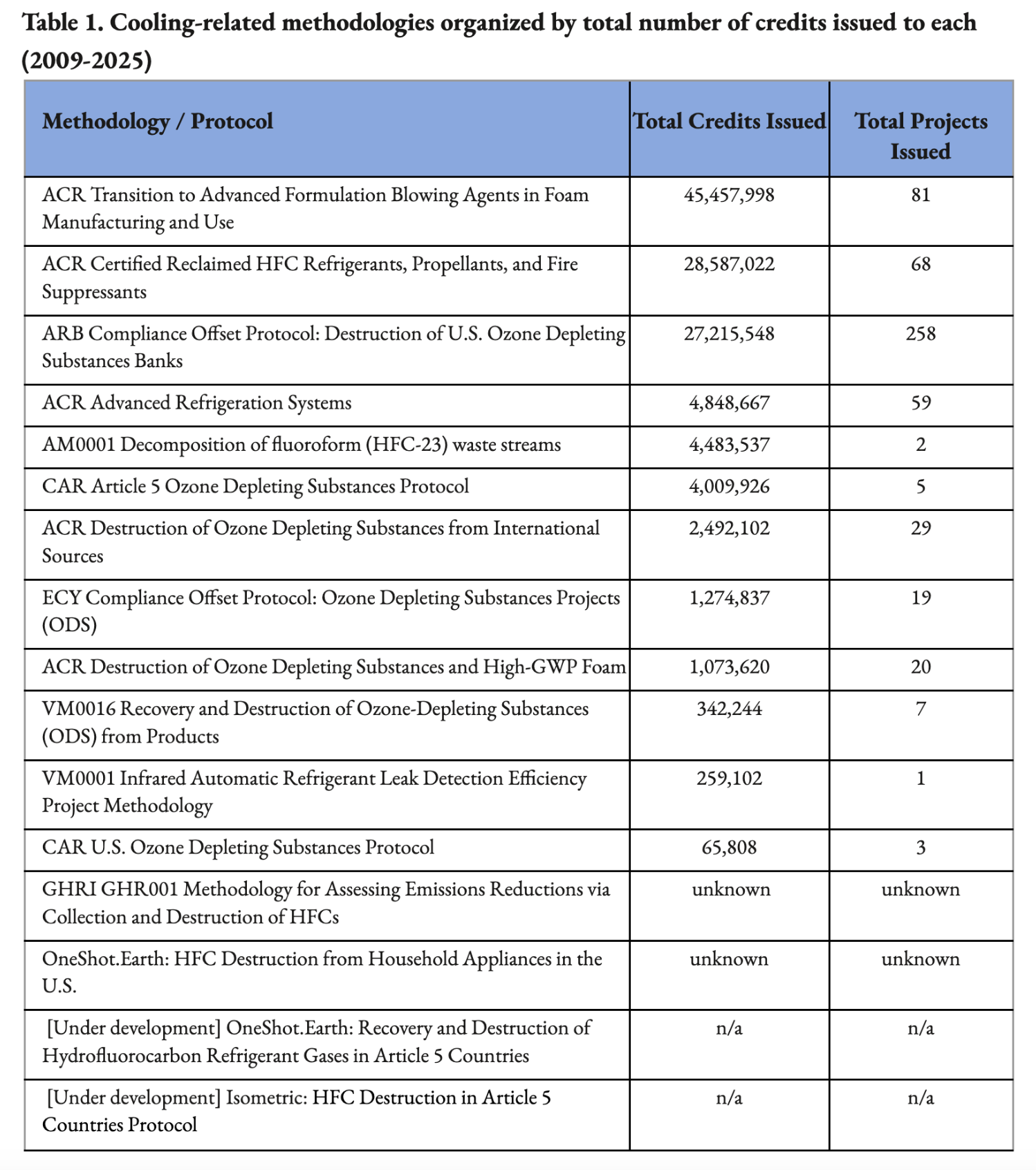

Table 1. Cooling-related methodologies organized by total number of credits issued to each (2009-2025)

Project Types & Credit Issuance

The cooling credit market has evolved from a narrow, destruction-driven market into a more durable and diversified mitigation landscape anchored in industrial and commercial transitions.

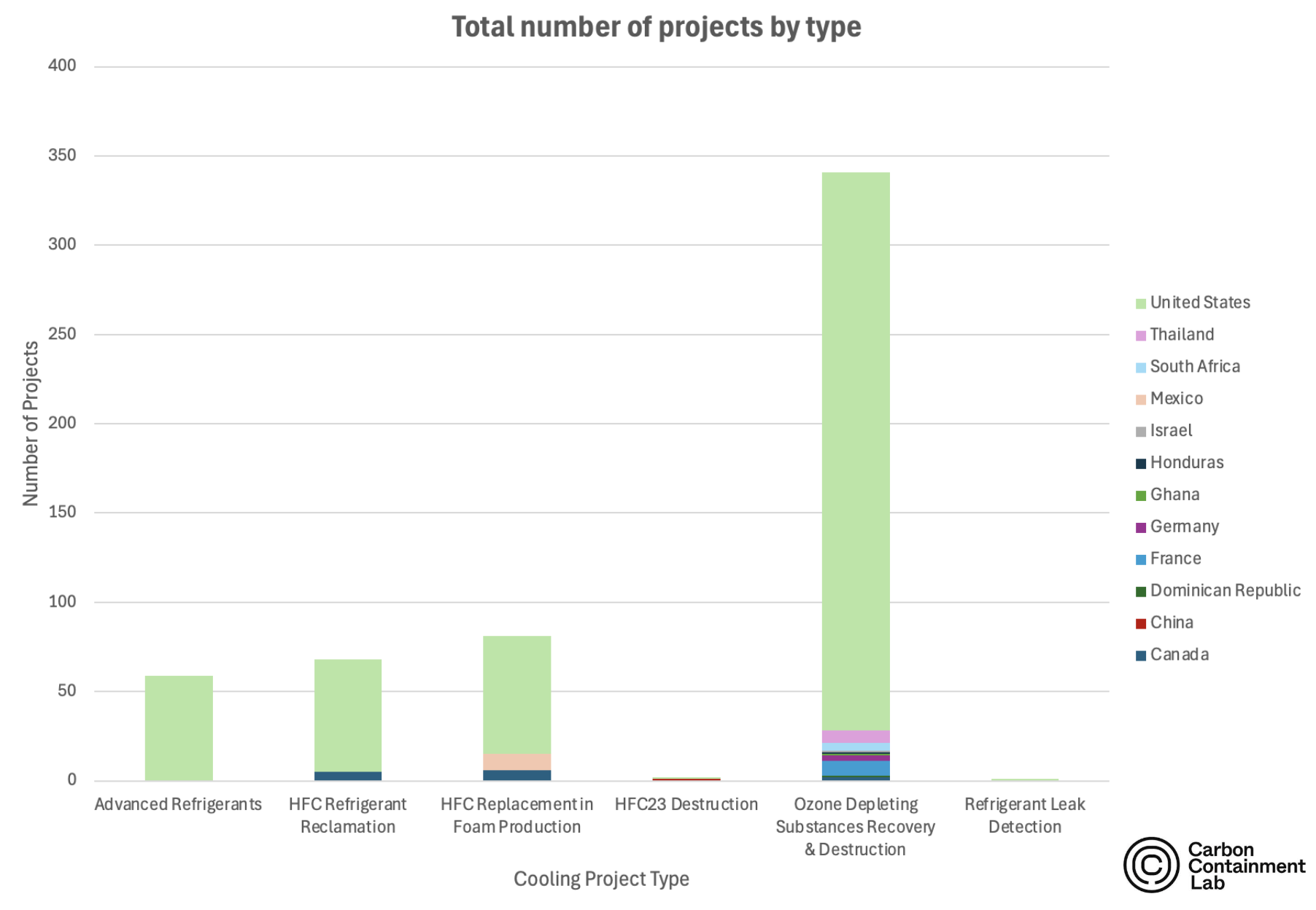

Of the 552 cooling projects reported by 37 project developers, roughly 93% are currently active or registered, with the remaining 7% (around 39 projects) in the registration pipeline. The U.S. hosts 91% of cooling projects, with the remaining 9% (49 projects) scattered across eleven countries, including Canada, Mexico, France, Thailand, South Africa, and Germany.

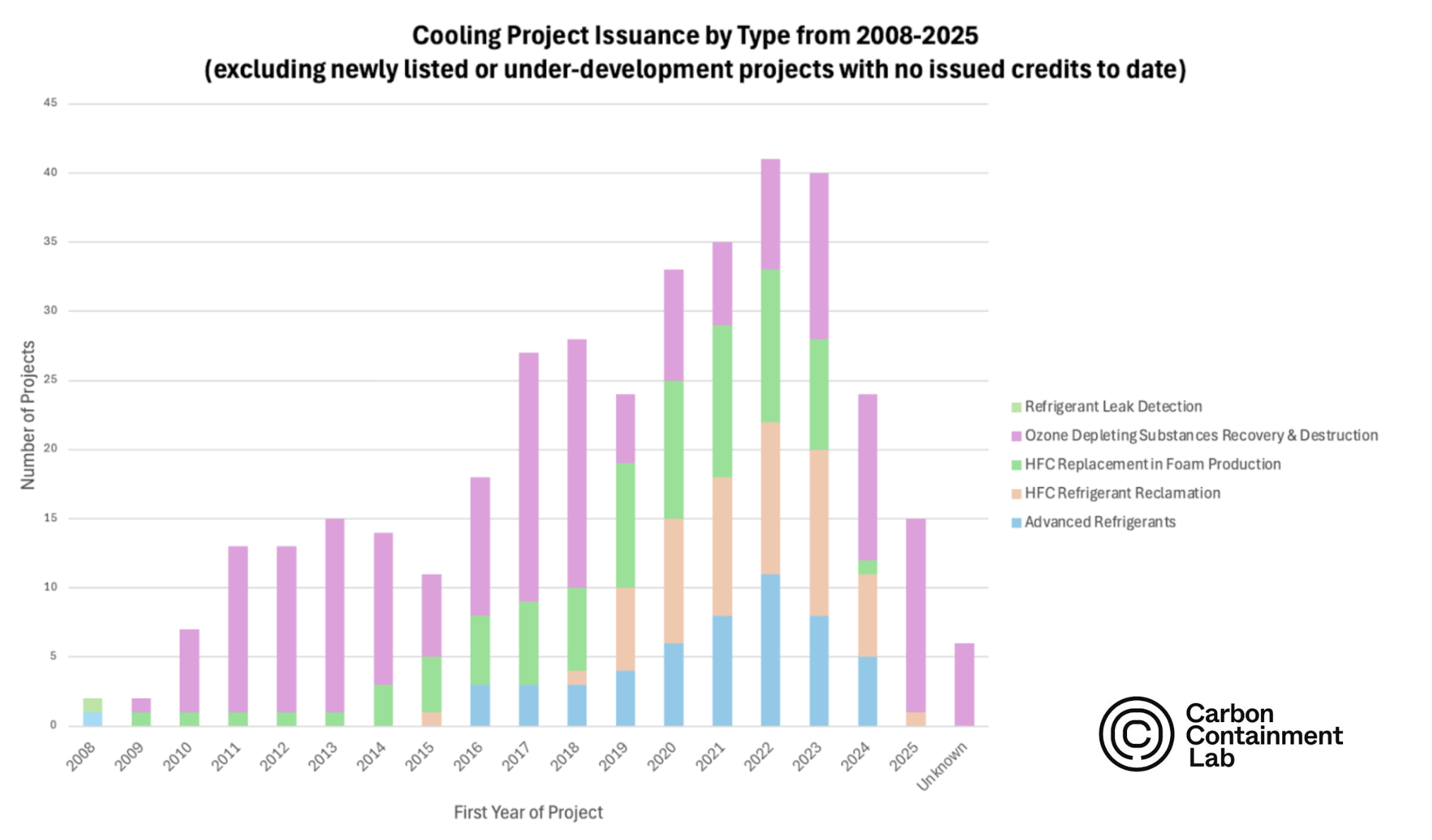

Figure 3. Total number of projects by type

ODS recovery and destruction represents approximately 62% of all projects and remains the dominant project type across both active and pipeline categories. By comparison, HFC-related pathways such as refrigerant reclamation (68 projects) and HFC replacement in foam production (81 projects) remain meaningful but secondary, while newer or more preventative approaches—such as advanced refrigerants and leak detection—represent only a small fraction of activity.

Figure 4. Percent share of cooling credits issued by registry

.png)

Of the total cooling credits issued to date, 76% (91,799,565 credits) have been issued through voluntary markets, with the remaining 24% originating from compliance programs. Compliance issuance is highly concentrated — credits are issued primarily by the California Air Resources Board (ARB) offset program and Washington State’s compliance market. Article 6.2 projects are starting to show up, though no cooling-related projects have been reported to date.

Looking at project registration and credit issuance trends over the years (figure 5 and figure 6), they strongly correlate with each other and reveal a clear three-phase evolution trajectory: (1) 2008-2012, a destruction-dominated emergence phase; (2) 2013-2019, a transitional diversification phase; and (3 )2020-2025, structural break and rapid expansion phase as explained below. There is a time lag between project development, registration, and finally credit issuance, such that actual numbers in 2025-2026 are expected to be higher than shown in the charts.

Figure 5. Number of currently registered projects by project type and start year

Phase 1. In the early years from 2008 to roughly 2012, project counts were low and almost entirely concentrated in ODS recovery and destruction. Credit issuance was volatile and heavily dependent on a narrow set of high-intensity methodologies. These early projects reflect Montreal Protocol-linked mitigation opportunities, with limited experimentation beyond destruction-based approaches.

Phase 2. From around 2013 to 2019, total project registrations increased steadily, still dominated by ODS recovery and destruction but with the first visible emergence of other project types. HFC replacement in foam production and, to a lesser extent, HFC refrigerant reclamation began to appear, indicating early movement toward process substitution rather than end-of-pipe destruction. Total credit issuance stabilized at moderate levels and gradually declined after the mid-2010s. This pattern is consistent with a maturing ODS project pipeline combined with limited scale-up of new cooling methodologies. The relative flatness of issuance suggests weak expansion in demand and lingering regulatory uncertainty in voluntary carbon markets. This period marked a transitional phase in which developers started responding to shifting regulatory signals and early expectations around HFC phase-downs, but the market remained structurally reliant on established methodologies.

Phase 3. A more pronounced diversification in both project types and credit issuance occurs from 2019 onward, followed by a structural break and rapid expansion in 2020. Both project counts and credits issued rise sharply, and multiple categories scale simultaneously. HFC refrigerant reclamation grows rapidly, alongside sustained expansion in HFC replacement in foam production. Advanced refrigerants and refrigerant leak detection also become recurring components of new project registrations, suggesting broader engagement across the refrigerant lifecycle. Unlike earlier phases, this growth reflects widespread adoption across manufacturing and refrigerant lifecycle management rather than isolated project types.

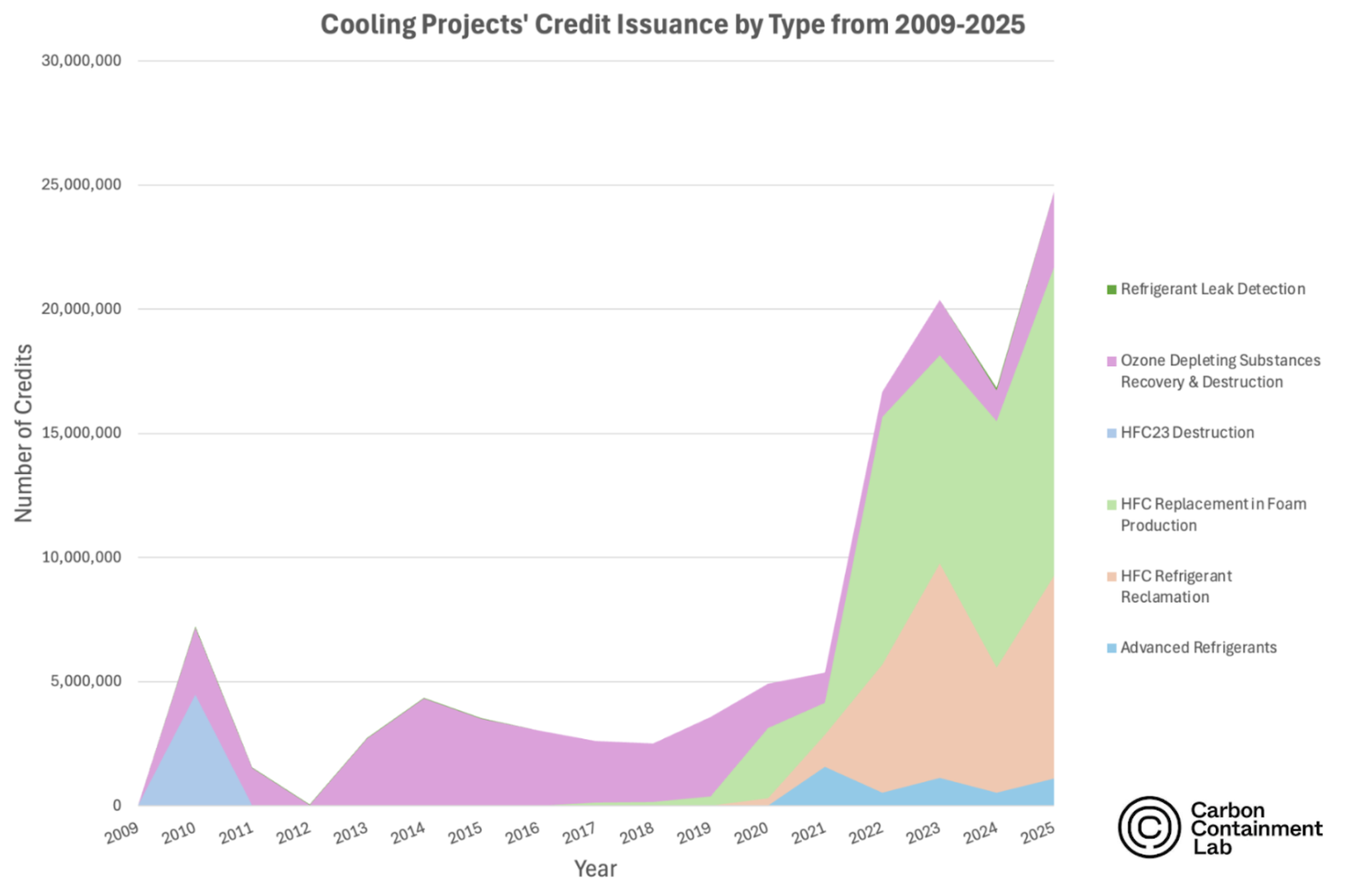

Figure 6. Credit issuances by project type and year

The composition of credit-types also changed fundamentally over time. Prior to 2020, issuance was overwhelmingly driven by destruction-based activities characterized by high credit intensity, low project counts, and sensitivity to regulatory changes and muted demand. After 2022, replacement and reclamation activities dominate, signaling a closer alignment with real-economy interventions and long-term decarbonization pathways. This shift mirrors broader policy dynamics, including the influence of the Kigali Amendment and growing corporate attention to supply-chain and Scope 3 emissions.

Credit Retirements

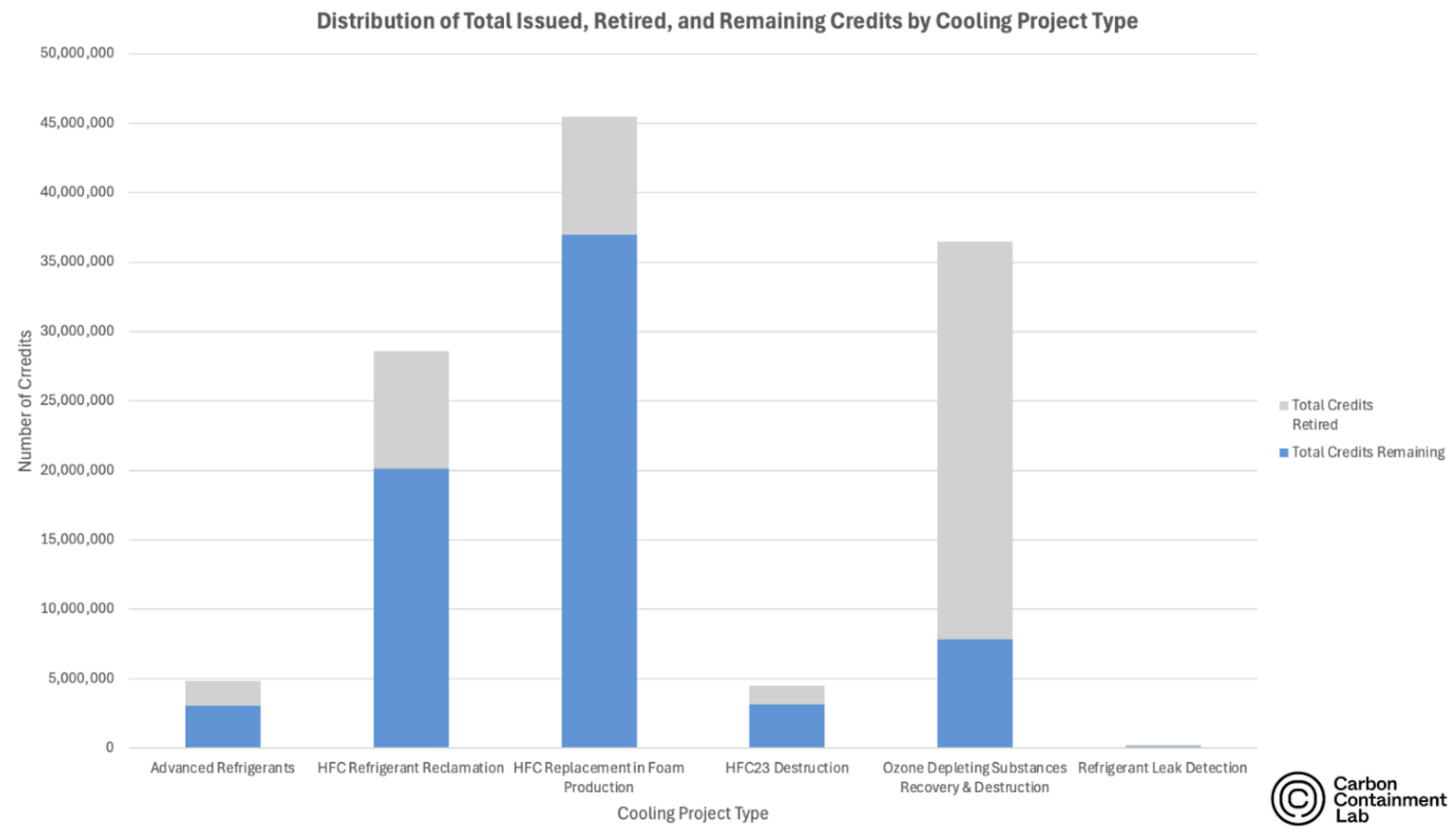

The distribution of issued, retired, and remaining credits reveals stark heterogeneity across cooling project types.

Retirement is the final, permanent removal of a carbon credit from circulation, ensuring it cannot be traded, resold, or reused, which signifies that the emission reduction (typically 1 tonne of CO2 e) has been officially claimed to offset a buyer’s emissions. Retirement is crucial to prevent double-counting, where the same climate benefit is claimed by multiple parties. Analyzing the percentage of remaining credits also helps to infer the potential number of credits available to purchase today that are still in circulation - or - that are being bought and held by buyers to offset future emissions.

Figure 7. Issued, retired, and remaining credits by project type

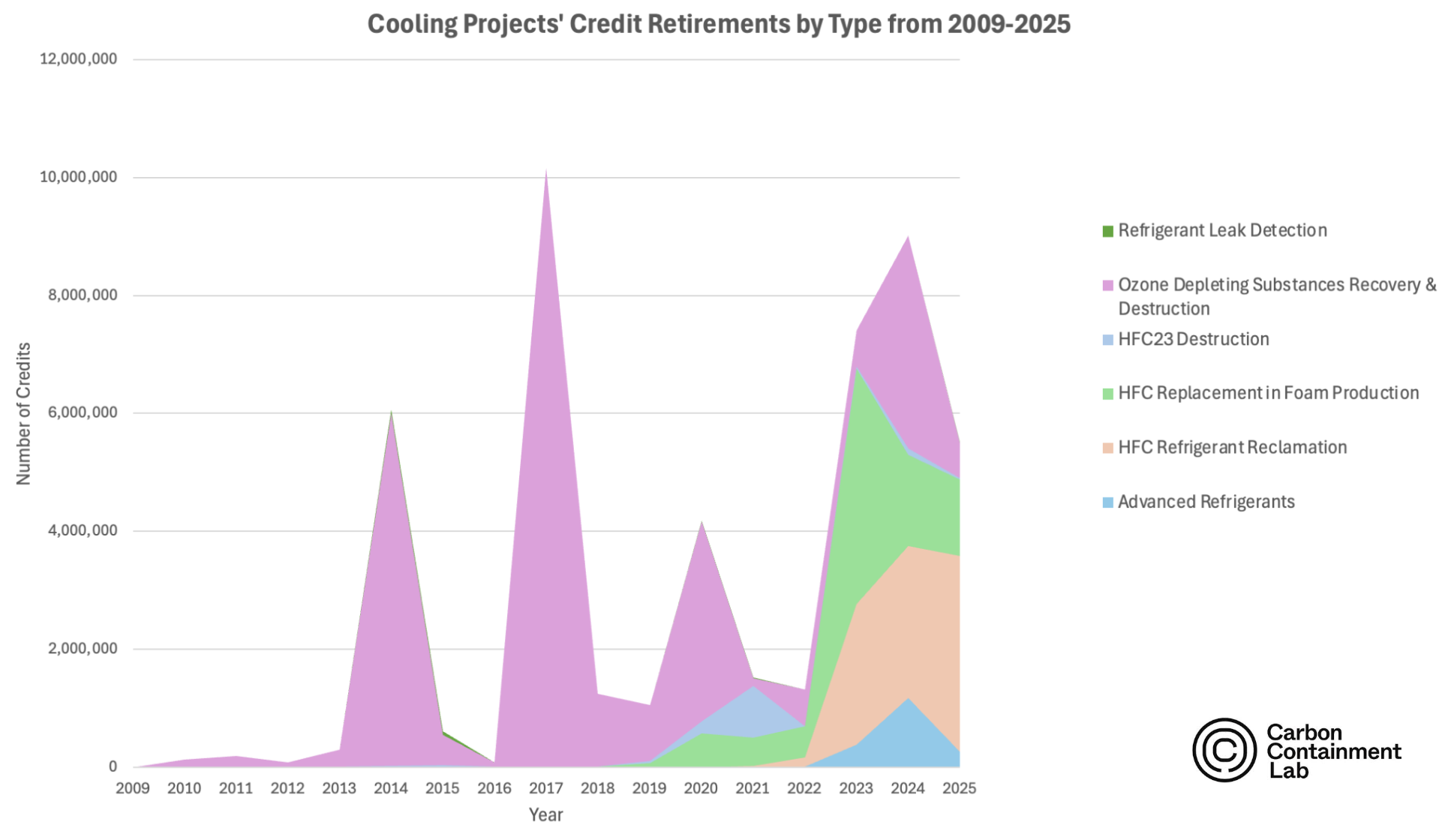

Credit retirements are dominated by ODS recovery and destruction, even though these projects account for a smaller share of remaining credit volumes. By contrast, HFC replacement in foam production and HFC refrigerant reclamation show substantial stocks of unretired credits. Analyzing the trends in cooling project credit retirements by year reveals a sharp acceleration in the retirement of credits from HFC-focused projects beginning in 2022.

Figure 8. Credit retirements by project type and year.

Looking Forward

Taken together, these patterns suggest that cooling mitigation in voluntary carbon markets was historically anchored in the rapid drawdown of legacy ODS stocks, whereas future mitigation potential will increasingly hinge on the sustained issuance and retirement of credits from HFC-focused project types.

Cooling currently represents an active but relatively small segment of both voluntary and compliance carbon markets. We expect more growth with multiple tailwinds supporting this view:

Corporate and institutional actors are intensifying efforts to meet 2030 climate targets, expanding demand for high-impact, relatively lower cost abatement options such as cooling and refrigerant-related credits.

An increasing number of high profile voluntary buyers such as Google are incorporating superpollutant mitigation into their portfolios, which in turn is incentivizing greater participation from project developers.

New methodologies and market channels are emerging across registries such as OneShot.Earth’s Open Carbon Protocol, the Global Heat Reduction Initiative, and Isometric; through platforms like Terraset, as well as through Article 6 mechanisms, which are expected to support growth in project issuance, purchasing, and retirement.

Compliance schemes are expected to drive demand broadly for carbon credits; for example, CORSIA is expected to add demand for around 78 million credits in 2026 across all project types according to Abatable's new report. While only a subset of programs are eligible that have cooling related credits today, we expect this to grow in future years as more programs and project types become eligible.

Independent rating agencies such as Calyx, BeZero, and Sylvera are now actively covering - and rating as high quality - cooling and refrigerant projects, improving market transparency and buyer confidence.

Legacy ODS stocks are declining, and destruction capacity remains constrained—suggesting a gradual shift away from finite ODS bank destruction toward more scalable, operational interventions involving HFCs.

Awareness is growing amongst stakeholders as to anticipated growth in the cooling sector, the need for resilience to withstand extreme heat events, as well as the climate impacts of cooling’s energy footprint and HFCs. We believe these drivers will raise the likelihood of policy and action on expanding recovery, reclamation, and lifecycle-based mitigation activities.

Future CC Lab briefs will project different growth scenarios for each cooling project type—stay tuned.